Cyber underwriters know the problem well. Underwriting questionnaires (UWQs) use different terms. Teams interpret the same answer in different ways. As a result, similar applicants can produce very different underwriting signals. ENISA has described questionnaires as an important way to estimate a customer’s cyber posture and compare applicants, while also noting the lack of a common assessment language. (ENISA)

That is the “translation tax” that a harmonized maturity approach is meant to reduce.

This post is an insurance-focused companion to:

- The original DeNexus blog on harmonizing OT cyber maturity models

- The related technical whitepaper on the OT Cybersecurity Maturity Journey (OT CMJ), and

- The broader DeNexus blog on maturity model use-cases.

Why insurers should care about harmonized maturity

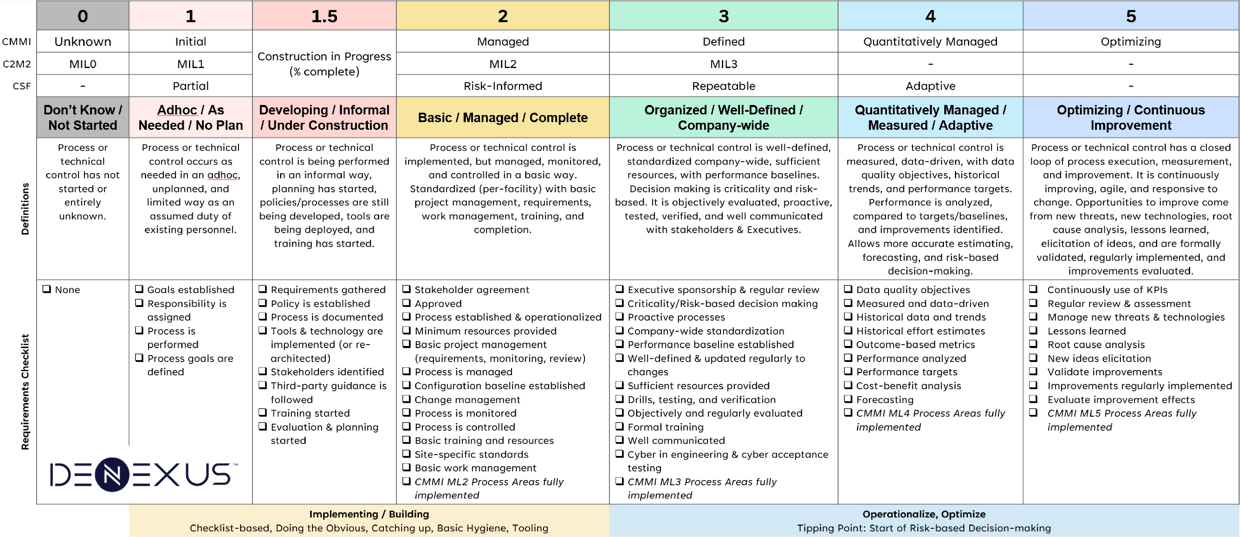

Higher cybersecurity maturity usually means a program is moving from ad hoc and reactive toward managed and proactive. That matters to insurers.

A low-maturity program is less likely to perform well under stress. Stress can come from a real cyber event, staff turnover, a shutdown, or a major operational upset. In those moments, weak processes tend to break down. When that happens, more risk can transfer to the insurer.

There is also a language problem. The applicant may use one maturity model. The underwriter may use another. One side may be optimistic. The other may be conservative. If they are not using the same measuring stick, the result is noise.

Higher maturity reduces that noise. It usually means stronger process discipline, better resilience, and more reliable execution. Mature programs are often better at detecting, containing, and recovering from cyber events. They are also less exposed to gaps caused by staff turnover or weak change control during outages and maintenance windows.

DeNexus has reconciled and harmonized multiple existing maturity models into one framework, revealing the methodology in the public domain, that can be adopted or revised by anyone.

A harmonized maturity layer like OT CMJ (i.e., DeNexus’ technical paper reconciling and harmonizing maturity models) gives underwriters a way to:

- normalize different UWQ language into one maturity signal,

- benchmark customers against peers, and

- turn maturity into more defensible underwriting decisions.

Below are five insurance use-cases that come from having a maturity scale that is more standardized, more consistent, and more defensible.

Use-case 1: Build peer baselines from anonymized UWQs

Problem

UWQs create a lot of data, but not always a lot of usable signal. Different carriers and brokers ask similar questions in different ways. Different underwriters may score the same answer differently. That makes peer comparison hard.

How harmonized maturity helps

DeNexus’ efforts to reconcile and harmonize maturity models (aka., OT CMJ) provides a common backbone. It translates varied UWQ answers into consistent maturity outcomes. That makes the data more useful for benchmarking and peer analysis.

Implementation

- Group anonymized submissions into comparable cohorts, such as sector, company size, OT footprint, number of sites, and remote access model.

- Build a mapping library from each UWQ question to a capability, a maturity requirement, and an evidence expectation.

- Score each submission against the harmonized maturity model.

- Compute peer percentiles, such as the 25th, 50th, and 75th percentile, by capability and by cohort.

Result

The underwriter can say, “This account is at the 20th percentile in recovery readiness for its peer group,” rather than, “They say they have backups.”

Use-case 2: Improve pricing, deductibles, retentions, and limits

Problem

Pricing and structure often rely on broad rating factors and underwriter judgment. Without a consistent security signal, those decisions can become coarse or subjective.

How harmonized maturity helps

A maturity percentile can become a defensible underwriting input. A harmonized model makes it easier to use security posture in a repeatable way.

Implementation

- Identify the capabilities that matter most to loss severity for the coverage being written.

- For business interruption, focus on restore testing, operating resilience, and segmentation.

- For extortion, focus on identity and access, monitoring, and response execution.

- For systemic exposure, focus on shared platforms and third-party access governance.

- Define percentile bands, such as below the 25th percentile, between the 25th and 75th percentile, and above the 75th percentile.

- Use those bands to guide:

- deductibles and retentions,

- business interruption waiting periods, (Society of Actuaries)

- limits and sublimits, and

- special conditions for low-maturity outliers.

- Track claims and loss experience by maturity band over time.

Outcome

The underwriter gets a rating logic that is easier to explain to brokers, managers, and supervisors.

Use-case 3: Turn post-bind risk engineering into a measurable plan

Problem

Many carriers offer post-bind services or risk engineering support. But the recommendations are often broad and hard to measure. At renewal, the discussion can fall back to opinion instead of evidence.

How harmonized maturity helps

A harmonized maturity model makes improvement measurable. Instead of saying, “Improve backup practices,” the insurer can say, “Move recovery capability from Level 1.5 to Level 2 and provide these specific artifacts as evidence.”

Implementation

- Bind the risk with a harmonized maturity profile.

- Pick the three to five maturity gaps that are most linked to severity for that class of business.

- Issue a post-bind improvement plan that includes:

- the target maturity change,

- the OT CMJ requirements to be met,

- the evidence required, and

- the validation steps and timeline.

- Tie renewal discussions to verified progress.

Outcome

Risk engineering becomes more concrete. Renewal discussions become more evidence-based.

Use-case 4: Standardize UWQs and clarify question intent

Problem

Customers often receive many questionnaires with overlapping but inconsistent questions. At the same time, carriers update UWQs as threats change. Over time, that can increase fragmentation instead of reducing it. (ferma.eu)

How harmonized maturity helps

OT CMJ can act as a stable “intent layer.” It defines what the underwriter really needs to know, even if different teams ask the question in different words.

That means:

- stable maturity requirements,

- flexible question wording,

- and clearer evidence thresholds.

Implementation

- Create a canonical catalog that maps each capability to a maturity requirement and evidence example.

- Map current UWQs to that catalog.

- Remove duplicate questions and identify missing areas.

- Standardize internal scoring first, even if external UWQs still vary.

- Over time, converge toward clearer and more consistent question sets.

Outcome

The insurer reduces friction for brokers and insureds while improving the quality of underwriting data.

Use-case 5: Build better underwriting signal from the same data you already collect

Problem

Insurers already collect UWQ data at scale, but much of its value is lost because the answers are not normalized. That limits how useful the data is for risk selection, pricing, and peer comparison.

How harmonized maturity helps

OT CMJ lets insurers reuse the data they already have. Pre-bind and post-bind UWQs can be translated into a common maturity language. That creates a stronger internal dataset for benchmarking, scoring, and portfolio learning.

Implementation

- Start with existing UWQs already in the underwriting workflow.

- Map historical answers into the harmonized maturity framework.

- Build internal peer baselines by cohort.

- Compare new customers to those baselines using percentiles.

- Use the results to support decisions on risk quality, pricing, and coverage structure.

Outcome

The insurer gets more value from existing underwriting data without needing to replace every questionnaire on day one.

Closing thought

Insurers and reinsurers are in a unique position. They can collect UWQ-based posture data at scale. They can anonymize it. And they can turn it into peer baselines that help separate better risks from weaker ones.

That is the core insurance value of OT Cybersecurity Maturity Journey, standardize the language, normalize the data, and turn cyber posture into underwriting signal—that is more standardized (shared definitions), more consistent (cross-walked), and more defensible (requirements-based and cumulative).

Download the reconciled and harmonized maturity technical paper